PE's Zombie Problem Isn't About Capital.

It's About Operations.

President, Zaruko

Table of Contents

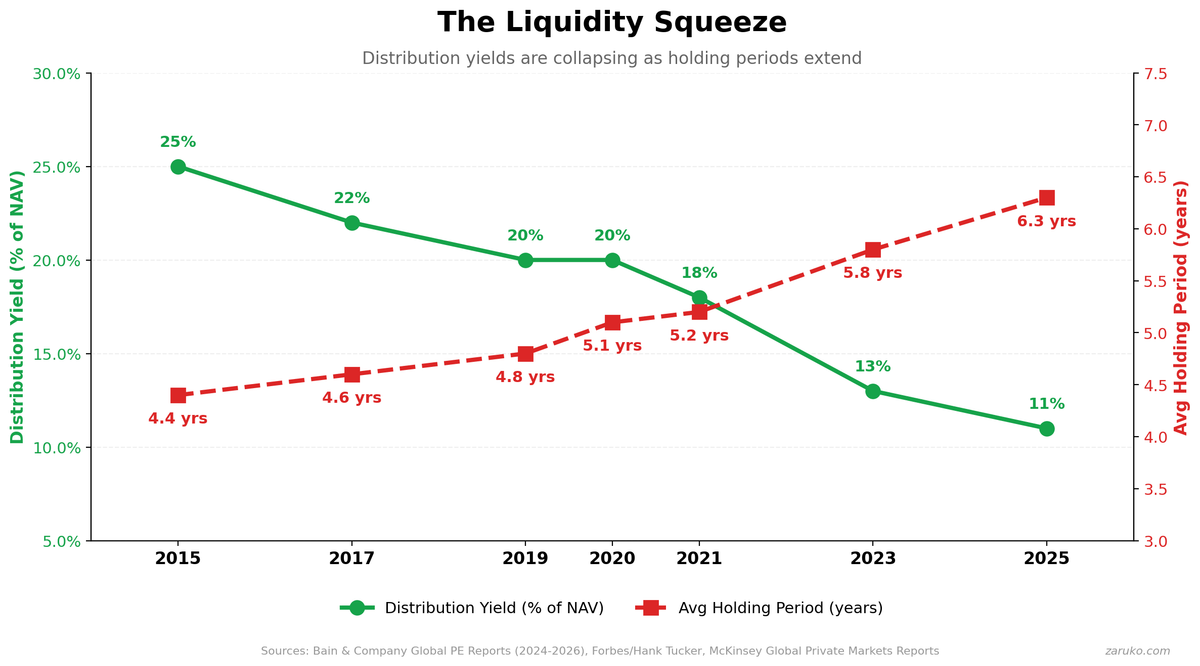

Forbes just published a list of 20 private equity firms that are either scaling back or treading water.1 The piece is excellent. Fundraising timelines stretched from 16 to 23 months. Distribution yields collapsed from 25%+ to 11%. Three-year PE returns trailing public markets by 11 percentage points.

But the article frames this almost entirely as a financial mechanics problem. Fundraising cycles. Fee structures. Continuation funds.

That framing misses the real question. Yes, higher rates and valuation gaps have slowed exits for everyone. But why are these firms' portfolio companies not worth acquiring even as the market recovers?

The data tells the story.

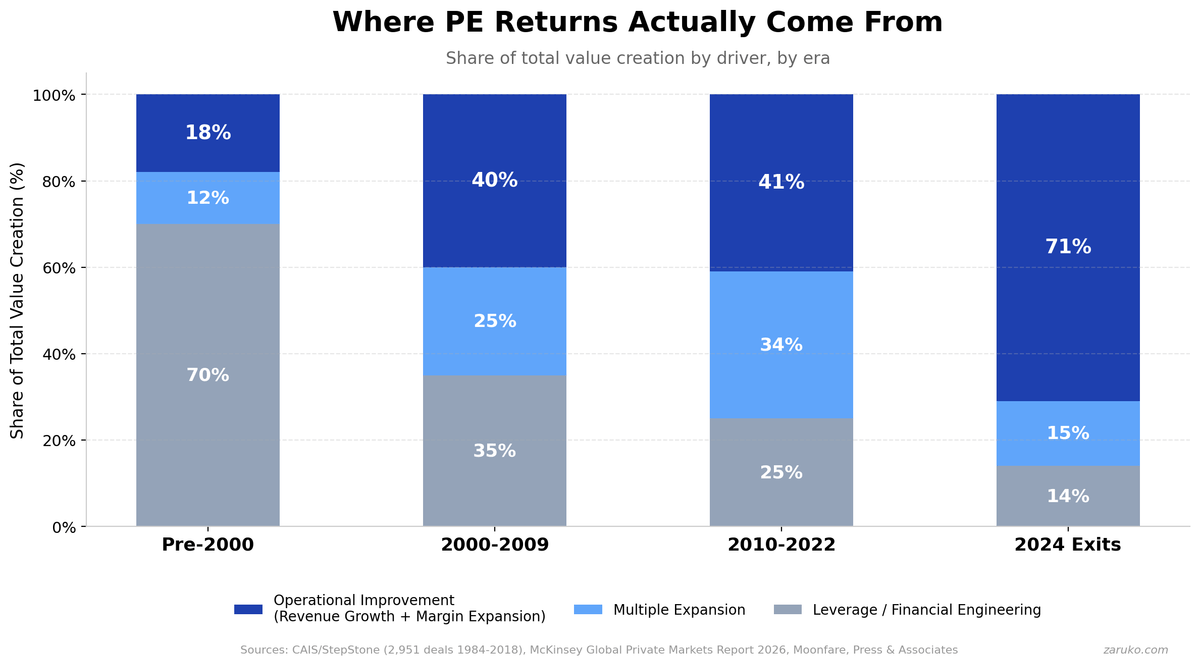

For deals entered after 2010 and exited before 2022, McKinsey and StepStone Group found that roughly two-thirds of PE returns came from leverage and multiple expansion.2 Only one-third came from actual operational improvement. Those two tailwinds are gone. Entry multiples hit a record 11.8x EBITDA in 2025. Debt as a share of entry multiples dropped from 44% to 37%.

Where PE returns actually come from. Operational improvement now drives 71% of value creation in 2024 exits.

The old playbook stopped working. The firms on the zombie list are the ones that never built a new one.

Meanwhile, the megafunds invested in operational capabilities. KKR has an internal operations group of roughly 100 professionals. Since 2010, operational improvements have accounted for 47% of PE value creation, up from 18% in the 1980s.3 McKinsey's 2026 report found that 53% of LPs now rank a GP's value creation strategy as a top-five factor in selecting a manager.2

LPs aren't withholding capital because they've lost interest in PE. 70% plan to maintain or increase allocations. The capital is flowing to firms that know how to make companies better, not just hold them.

The liquidity squeeze. Distribution yields have collapsed while holding periods keep extending.

Most midsize PE firms never made this investment. They know how to source deals, structure debt, and negotiate terms. What they don't know is how to make a portfolio company operationally better in ways that show up in revenue and margin. That's a different skill set.

A portfolio company that hasn't improved after six years of PE ownership isn't going to become more attractive after eight. Continuation funds buy time. They don't fix the problem.

This isn't a fundraising crisis. It's a value creation crisis. And it won't resolve itself.

Sources

- Forbes, "Why Private Equity Is Suddenly Awash With Zombie Firms" by Hank Tucker. Fundraising timelines stretched from 16 to 23 months; distribution yields collapsed from 25%+ to 11%; three-year PE returns trailing public markets by 11 percentage points. ↑

- McKinsey, Global Private Markets Report 2026. Entry multiples hit 11.8x EBITDA in 2025; debt share dropped from 44% to 37%; 53% of LPs rank value creation strategy as a top-five GP selection factor; 70% of LPs plan to maintain or increase allocations. ↑

- Gain.pro, PE Value Creation Report 2025; CAIS/StepStone Group (2,951 deals 1984-2018); Press & Associates; Moonfare. Operational improvements account for 47% of PE value creation since 2010, up from 18% in the 1980s; 71% of value creation in 2024 exits came from operational improvement. ↑

Frequently Asked Questions

Why are so many private equity firms becoming zombies?

PE zombie firms are stuck because the two traditional drivers of PE returns (leverage and multiple expansion) have stalled. Entry multiples hit a record 11.8x EBITDA in 2025 and debt as a share of entry multiples dropped from 44% to 37%. Distribution yields collapsed from 25% to 11% while holding periods stretched from 4.4 to 6.3 years. The firms on the zombie list never built operational value creation capabilities to replace the old playbook.

What drives private equity returns today?

Operational improvement now accounts for 71% of value creation in 2024 exits, up from just 18% pre-2000. Leverage and multiple expansion, which historically drove the majority of PE returns, have become much less significant as interest rates rose and entry multiples peaked. McKinsey's 2026 report found that 53% of LPs now rank a GP's value creation strategy as a top-five factor in selecting a manager.

How should PE firms adapt to the current market environment?

PE firms need to invest in operational capabilities that make portfolio companies genuinely better, driving revenue growth and margin expansion rather than relying on financial engineering. 70% of LPs plan to maintain or increase PE allocations, but capital is flowing to firms that demonstrate real operational value creation. Continuation funds buy time but do not fix the underlying problem.

Continue Reading

First Principles of AI

Ten foundational principles for evaluating AI claims and making better decisions.

The Simple Rule that Separates AI Winners from Everyone Else

Automate the repeatable. Keep humans on the judgment calls.

Before You Bet 90 Days on AI: An Operator's Scoping Checklist

A six-point checklist for scoping AI projects that produce results instead of expensive lessons.

Building operational value in your portfolio?

I help mid-market companies turn operational improvement into measurable business results. Let's talk.

Let's Talk